TerrieLea Blueitt thought her home would sell in a week. But in one year, she said, maybe ten people have come to see it. And data out of the state’s Realtor association shows the housing market is cooling in general.

https://007re.net/wp-content/uploads/2025/09/Recession-or-a-righting-Marylands-housing-market-is-cooling-off.jpg6821024Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-20 12:28:152025-09-20 12:28:15Recession or a righting? Maryland’s housing market is cooling off

As summer winds down and fall rolls in, Newport’s real estate market is entering a pivotal phase — one that could set the tone for the end of the year. Between shifts in inventory, buyer behavior, and pricing, both buyers and sellers are seeing changes that are already starting to shape the market.

Key Trends to Watch This Fall

1. Prices Up, But Homes Taking a Bit Longer to Move While values are rising, median days to go pending are hovering in the high 30s. That suggests buyers are being more selective, and homes aren’t flying off the market quite as fast as during peak summer frenzy.

2. Supply is Tight, Especially Under $1 Million Inventory remains constrained, especially in more affordable price bands. Homes in the $400,000-$700,000 range are showing strong demand, but choices are limited. Sellers in this range are in a good position — with the right pricing and presentation, homes tend to attract serious interest quickly.

3. Luxury & Second-Home Market Activity Remains Strong Newport has long been a destination for second homes, vacation properties, and luxury buyers. As some homeowners who benefited from equity gains over recent years opt to sell, there’s an increase in high-end listings. Also, with seasonal moves (snowbirds, etc.), many buyers are actively looking now to lock in before winter.

4. Fall Lifestyle & Design are Playing a Big Role It’s not just about location or square footage this year. A recent trend: buyers are looking for homes that evoke comfort, warmth, and lifestyle. Think: cozy interiors, updated kitchens, flexible spaces (home offices, studios), outdoor areas that work even as the weather cools. Homes that present well in autumn — both inside and out — are standing out.

5. Interest Rate Sensitivity & Buyer Timing Potential buyers are keeping a close eye on mortgage rates and economic signals. With a possibility of interest rate changes, many want to lock something in now rather than wait. Sellers, similarly, are weighing whether to list now to capture the current demand or wait, hoping for more favorable conditions. Timing will matter a lot.

What This Means for Buyers & Sellers

For sellers: Fall can still be a great season to list — especially if your home is well-staged, properly priced, and highlights what people value this time of year (comfort, ambiance, and lifestyle amenities). With less competition than summer, you might stand out more.

For buyers: Go in with patience and a clear vision. Be ready to move quickly if the right property shows up. Even if inventory is tight, there are opportunities if you stay flexible on style, timeframe, or neighborhoods.

For both: It’s a market that rewards preparation. Whether you’re getting your home ready to show or getting your financing lined up, the folks who are prepared tend to come out ahead. Also, understanding micro-neighborhoods (Historic Hill, The Point, etc.) and their seasonal nuances can give you an edge.

Looking Ahead: What Could Tip the Balance?

Any moves from the Federal Reserve or changes in mortgage rates could shift affordability quickly.

New listings entering the market could ease supply constraints — especially in sought-after price ranges.

Seasonal patterns: as winter nears, fewer people move, fewer homes list — so the window for action before things slow is narrowing.

If you’re considering buying, selling, or just curious where the market is headed, now is the time to engage with trusted local experts who truly know the Newport landscape.

Presented by The Dowd Team — your Newport real estate specialists. Reach out if you want a personalized market analysis, tips for staging, or guidance on timing your move.

Like Newport Buzz? We depend on the generosity of readers like you who support us, to help with our mission to keep you informed and entertained with local, independent news and content. We truly appreciate your trust and support!

https://007re.net/wp-content/uploads/2025/09/1758358180_Heading-into-Autumn-Whats-Hot-and-Whats-Changing-in-the.png500750Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-20 08:49:392025-09-20 08:49:39Heading into Autumn: What’s Hot (and What’s Changing) in the Newport Real Estate Market

BOSTON— As AI-driven investment surges and tech companies reimagine their real estate strategies, Boston continues to solidify its status as one of the top U.S. markets shaping the future of tech office activity, according to a newly released report by Colliers.

Analyzing 26 key U.S. markets, the report highlights Boston’s unique advantage in the national tech landscape. Armed with a powerful trifecta — a deep venture capital network, world-renowned universities, and a highly educated tech workforce — Boston is well-positioned to attract and retain high-value tech operations.

This position was further strengthened in March 2025, when NVIDIA announced the launch of its Accelerated Quantum Research Center in Boston, drawn by the city’s deep ecosystem of academic research, biotech innovation, and next-gen computing.

Venture Capital Surge, AI Dominance

Tech office markets are riding a new wave of momentum, driven by an explosion of venture capital investment — particularly in AI and quantum technologies. In the first half of 2025 alone, U.S. venture capital topped $120 billion, with AI accounting for a record 18.5% of all capital raised. Boston’s leading VC segments — biotechnology, drug discovery, and business/productivity software — remain at the core of this trend.

Talent & Workforce Advantage

Boston ranks among the top markets nationally for educational attainment, trailing only Washington, D.C. and San Francisco. This positions the city to compete for the next generation of tech talent as labor markets shift. While population and job growth surged in Sunbelt cities like Austin, Orlando, and Nashville, Boston remained a premium destination for high-wage, high-skill tech employment.

Office Market Outlook: Signs of Recovery

Despite a soft first half in 2025 — with negative net absorption and a vacancy rate averaging 19.6% across major tech markets — Colliers sees signs of stabilization. In fact, nearly 50% of tech leases signed this year represent new growth, a signal of renewed expansion.

Boston’s market is currently in a “key moment” phase — with rental rates bottoming out, indicating a likely upturn in the months ahead. While new developments have slowed, demand for premium office space remains strong, particularly from companies in life sciences and AI.

As the national tech sector begins to rebound and redefine workplace needs, Boston is not just holding its ground — it’s quietly leading the way.

(Source: Colliers, U.S. Top Tech Markets Report, September 2025.)

Related

Advertisement

https://007re.net/wp-content/uploads/2025/09/1758344855_Boston-Holds-Strong-as-National-Tech-Hub-Amid-Shifting-US.jpg19172560Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-20 05:07:352025-09-20 05:07:35Boston Holds Strong as National Tech Hub Amid Shifting U.S. Office Market, Says Colliers Report

Last year, South Florida’s housing market saw very little supply and higher demand. At the time, the real estate market saw sellers making massive profits off homes in a short timeframe.

Fast forward to one year later and there’s different story. The housing market is now seeing a new trend of sellers taking their homes off the market. South Florida is leading the nation in this new trend. According to Realtor.com, in the month of July, for every 100 homes posted for sale, 59 listings were removed in the Miami-Fort Lauderdale-West Palm Beach metro.

These listings were not posted for a short time. In the tri-county area, the average listing spent 88 days on the market. That is the longest amount of time compared to any other top metro. When compared to the national average, for every 100 homes only 21 are taken off the market and the average listing spent 58 days on the market. Real estate expert Bryan Gorrita says there are two major reasons why there are more sellers than buyers in today’s market.

The first is the cost of ownership. Insurance premiums and property taxes have risen and consumers don’t want to pay the extra costs.

“Sellers now are saying it doesn’t make sense for me to own this property, let me sell it and try to get the most that I can,” explained Gorrita. “The other thing is greed. They purchased their home five six years ago and they might have bought it for $300,000 and think they are going to get a million dollars.”

Gorrita’s point is what the Realtor.com report indicates. Less than 18% of homes have a reduction in price. This suggests, according to Gorrita, that sellers would rather wait it out then to sell.

“These prices that we are seeing is a product of what we saw during the Covid-19 pandemic. And, with the rush of people coming down here [South Florida], purchasing homes and relocating,” said Gorrita. “Now that we have had time after the pandemic, a lot of people who came from New York and other parts of the country have had to go back to their home state, and go back to their jobs, but the problem is that the prices haven’t accommodated.”

What does this shift mean for you? Gorrita says those looking for a place to live should consider the rental market, as he claims it’s slightly more affordable and you can negotiate price. Gorrita also advises that if you want to buy a home, look at the number of days it has been listed. If it’s been posted anywhere from 4 to 6 months there might be a reason.

“At the end of the day you don’t know what is going on, there might be a death in the family, they need to relocate, they need a bigger home, and at that point they might be more willing to adjusting their price and making a deal,” explained Gorrita.

The realtor also encourages potential buyers to negotiate. Gorrita says if you have a price in mind, don’t overspend and put in the offer you want.

https://007re.net/wp-content/uploads/2025/09/South-Florida-homes-are-being-pulled-from-the-market-at.jpg6751200Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-19 21:49:142025-09-19 21:49:14South Florida homes are being pulled from the market at highest rate in nation – NBC 6 South Florida

https://007re.net/wp-content/uploads/2025/09/Buyers-Have-the-Upper-Hand-in-Dallas039-Real-Estate-Market.webp.webp12001800Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-19 18:10:142025-09-19 18:10:14Buyers Have the Upper Hand in Dallas' Real Estate Market Today

There’s no doubt that commercial real estate, and especially the office market, is undergoing a seismic transformation, one that’s not likely to abate any time soon. A boom time of near-zero-interest-rate policy, abundant liquidity, and cap rate compression over the past decade has given way to a perfect storm-a wall of maturing debt, tightened lending conditions, and cratering property values-all amid higher interest rates that show no sign of returning to their pre-2022 lows.

The outlook for the office sector has been particularly negative. It’s a tale of two markets right now: roughly 30% of office buildings account for 90% of the vacancies and may never recover, while the other 70% have the chance to stabilize over time. Either way, the office market finds itself at an inflection point, much like the retail market as mall acquisitions were being financed.

It’s equally clear that this total reset won’t reverse itself any time soon as the cost of capital will remain elevated for the foreseeable future. Using a forward yield curve to track the U.S. 10-year Treasury, we can forecast yields rising from 4.46% in July 2025 to 5.78% in July 2035. Inflationary pressures will persist, and the historically accommodative monetary policy of the past decade will not spring back to life. The genie can’t be put back in the bottle.

This dislocation creates gaps in the market. Banks are growing skittish towards their exposure to office real estate, and in May the Federal Reserve Bank of St. Louis reported that banks’ CRE loan growth had plummeted to an 11-year low. The Federal Reserve Bank of New York has publicly warned that CRE risks will weigh on banks’ balance sheets for years to come.

A special situation strategy for a special situation

Under these circumstances, it is “special situation investing” that will win the day. Special situation investing comes from the hedge fund world, where it means stepping into moments of market dislocation where traditional capital isn’t available because of complexity and distress. At Peachtree, not all distress is created equal: we differentiate between cyclical stress (e.g., a hotel that needs a bridge loan through renovation) and structural obsolescence (e.g., challenged office assets that may never recover).

There’s an enormous appetite for this type of flexible capital. The private credit market has grown by 50% in the past four years, ballooning to $1.7 trillion with no signs of stopping. (Morgan Stanleyestimates the private credit market’s growth potential to leap to $2.6 trillion by 2029.) As banks grow increasingly wary of lending to CRE, private credit and special situations capital will no longer be sidelined as alternatives; the flexibility, speed, and dependability of these solutions will make them primary sources of funding.

Where traditional lenders are pulling back due to balance sheet pressure and concerns about the health of the office market, special situations investors will fill the void with preferred equity, mezzanine debt, bridge loans, and rescue capital. Investors will position themselves as problem-solvers for banks and sellers by acquiring non-performing loans and purchasing distressed debt, often at discounted pricing. At a time when many investors lack operational bandwidth and expertise, those who can close quickly and manage properties directly will have the edge. And as skyrocketing insurance premiums, labor shortages, and taxes drive up property expenses sharply, every dollar that can be saved by rigorous underwriting discipline and operational efficiency becomes precious.

All in all, the winners in this choppy period for the office market won’t be passive buyers or those who are still casting a backward look at pre-2022 conditions; the winners will be strategic operators willing to step into the gaps created by CRE’s seismic shift. Making lemonade out of lemons in this difficult environment will require keeping one eye on capital markets complexity and another on property-level operational challenges-and it will necessitate a willingness to fill the market’s gaps.

The entry points for special situations investors are attractive ones, and we’ll continue to see plenty of buzzy headlines about private credit as the newest “shiny object” on Wall Street. But make no mistake: most firms that have jumped on the private credit bandwagon recently lack the necessary infrastructure and true expertise to execute effectively. The investors who have spent years building durable and battle-tested teams across all cycles, good times and bad, are the ones who are prepared to reap today’s rewards.

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.

Fortune Global Forum returns Oct. 26-27, 2025 in Riyadh. CEOs and global leaders will gather for a dynamic, invitation-only event shaping the future of business. Apply for an invitation.

https://007re.net/wp-content/uploads/2025/09/Commercial-real-estates-seismic-transformation-is-creating-new-winners-and.jpg6001200Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-19 14:31:162025-09-19 14:31:16Commercial real estate’s seismic transformation is creating new winners and losers

Because you are coming from a location (Texas) covered by a Privacy Law, many of the features of TribLIVE.com, like videos and social media elements are disabled. If you wish to proceed to the site under those conditions (doing so will effectively opt you out of the sale of your personal data) click here. However you will not experience the full features of TribLIVE.com that rely upon third party networks that may require your personal data.

Click here to agree to experience the full features of TribLIVE.com and to opt in to the use of your personal data to provide that experience and advertising.

Bookmark this page to manage your preferences any time in the future.

If YOU ARE NOT visiting us as a resident of Texas? Please update your location to ensure you are presented with the best experience.

https://007re.net/wp-content/uploads/2025/09/Notice-of-Privacy.png70212Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-19 10:52:162025-09-19 10:52:16Notice of Privacy

Housing This section of the BDN aims to help readers understand Maine’s housing crisis, the volatile real estate market and the public policy behind them. Read more Housing coverage here.

Open houses, which were once considered a common part of the home sale process, have fallen by the wayside in recent years due to changes in Maine’s real estate market.

While open houses are still useful in some cases, real estate agents agree they aren’t needed in order to sell a property. The practice was primarily killed by new technology, the pandemic and Maine’s frenzied housing market.

The dwindling number of open houses across the state is one of many ways the state’s housing market — and housing marketing strategies — have transformed in a few short years. It also points to the ripple effects of the global pandemic that are still being felt today.

The state’s housing market has cooled considerably from the fever pitch it reached in the heart of the pandemic, but properties are still changing hands quickly. That doesn’t leave much time for brokers to schedule and hold open houses, said Jeff Harris, Maine Association of Realtors president and a broker at Harris Real Estate in Farmington.

Homes sat on the market for an average of nine days before being snatched up in August 2021, according to Redfin. Last month, properties were available 41 days before closing.

“Open houses would be scheduled and everybody would put them in their calendars, then a day later you’d get a note saying the house is under contract and the open house is canceled,” said Chris Lynch, president and owner of Legacy Properties Sotheby’s International Realty, which has six offices throughout the state.

But open houses were becoming less common long before the pandemic. As the housing market recovered from the recession that hit the U.S. in 2007, houses were selling faster and the habits of house hunters were shifting.

The pandemic then halted open houses altogether in 2020, as larger indoor gatherings weren’t allowed. When they returned, guests were required to wear face masks, gloves and even shoe coverings, Lynch said.

While the slow return of open houses was rocky at first, Lynch said their absence showed they weren’t actually needed.

“We found that there really wasn’t a meaningful correlation between open houses and actually selling the property,” Lynch said.

Open houses draw mostly “looky loos” who only want to take a peek inside a home and aren’t interested in buying it, Lynch said. Sellers often decide against holding an open house in order to avoid inviting those people in, especially when an open house doesn’t guarantee an offer.

Most serious buyers work with a real estate agent to find a house, which allows them to schedule private showings of homes, Harris said. Shoppers usually prefer having time and privacy to walk through a home alone.

“We have a lot of technology at our fingertips that allow us to set up showings easily,” Harris said. “We get on our iPhones, type in the address, it goes right to the listing broker and we request a showing for, say, 11 on Thursday.”

Additionally, technology has advanced to allow interested buyers and nosey neighbors alike to see a home’s interior without ever stepping foot inside, negating the need for an open house.

Online listings usually include dozens of photos that show every inch of a property’s interior and exterior. In some cases, virtual tours of a property take the viewer through the home, which gives a clear idea of the building’s layout.

“With the new technology, now when people come into a home for the first time, it’s almost like a second showing,” Lynch said. “Interested buyers look behind all the doors and cabinets that were closed in the pictures because they already know everything that was exposed.”

While open houses have become less common and aren’t necessary, Harris said they can still be useful in some cases. For example, an open house often generates interest and could get a seller multiple offers, especially for a clean, turnkey home in a desirable neighborhood.

Open houses can also be useful for out-of-state buyers who can ask local family or friends to attend an open house in their place and provide feedback, Lynch said.

https://007re.net/wp-content/uploads/2025/09/Maines-real-estate-market-shifts-away-from-open-houses.jpg8001200Nemahttps://007re.net/wp-content/uploads/2021/11/007-logo.jpgNema2025-09-19 07:12:562025-09-19 07:12:56Maine’s real estate market shifts away from open houses

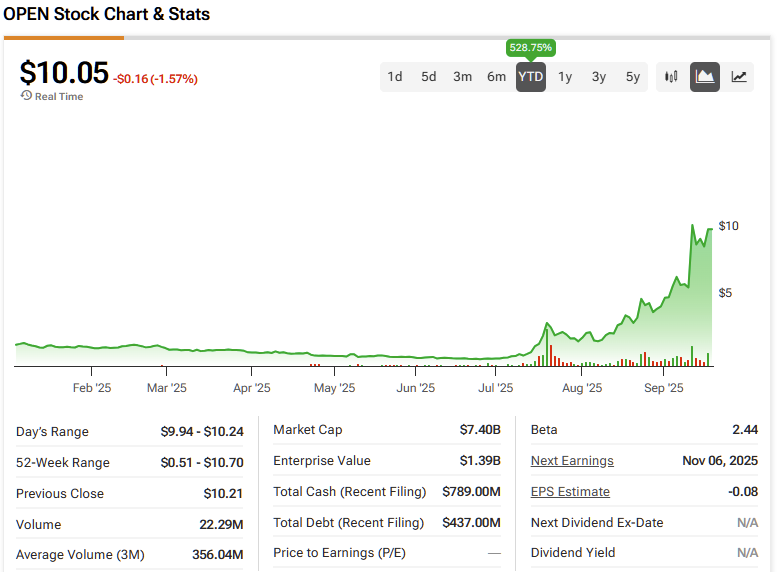

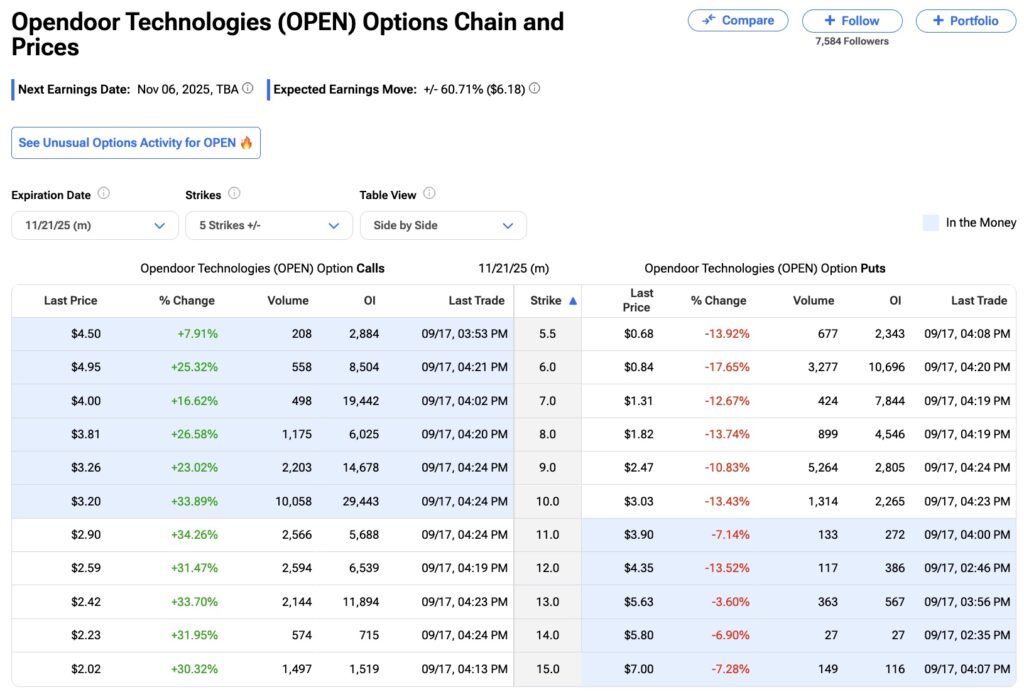

Opendoor Technologies (OPEN) has been on a tear, with shares soaring more than 525% year-to-date as retail investors fuel a powerful rally. Several catalysts are driving the surge: an activist investor increasing their stake, a leadership change aimed at turning around the business model, and a friendlier rate environment breathing life back into the housing market. Even the likes of Warren Buffett have been seen building out their beachheads in the real estate sector.

Elevate Your Investing Strategy:

Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Separating hype from actual fundamental improvements is challenging, especially since Opendoor has never reported a profitable full fiscal year since its inception in 2014. For that reason, I see OPEN more as a trading vehicle than a long-term investment. Momentum shows no signs of cooling, particularly among retail investors, and I expect high volatility that could create trading opportunities at least until the following earnings report in early November, which may serve as the next key inflection point under the new C-suite.

Given this backdrop, a speculative Buy rating for OPEN may still be warranted, but it should ideally be paired with a hedging strategy—such as options—to mitigate downside risk.

What Essentially Moves OPEN Stock

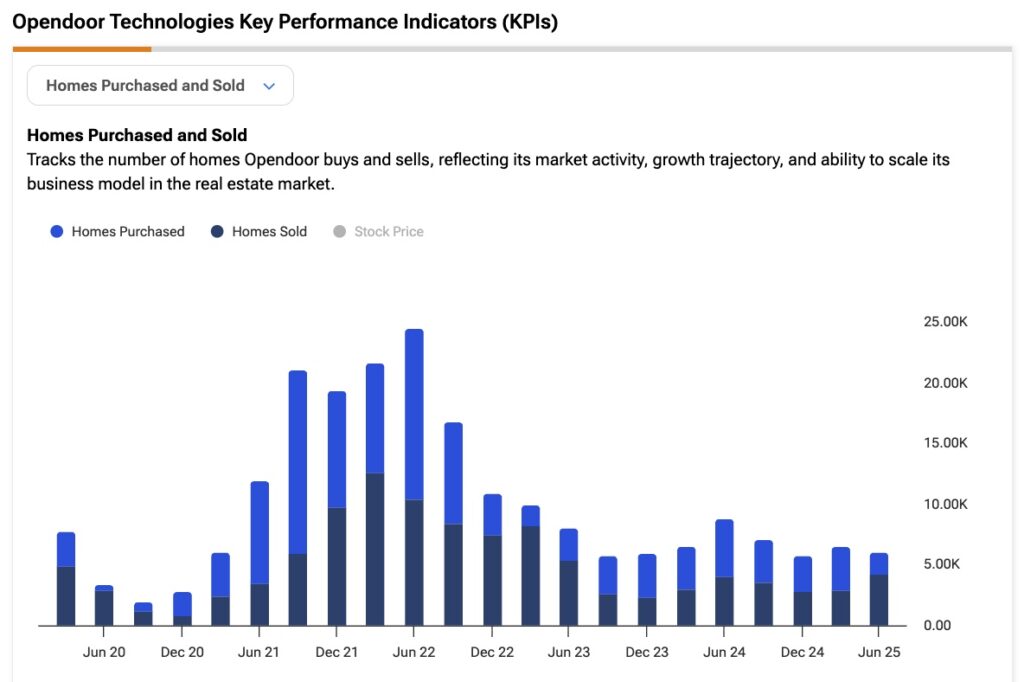

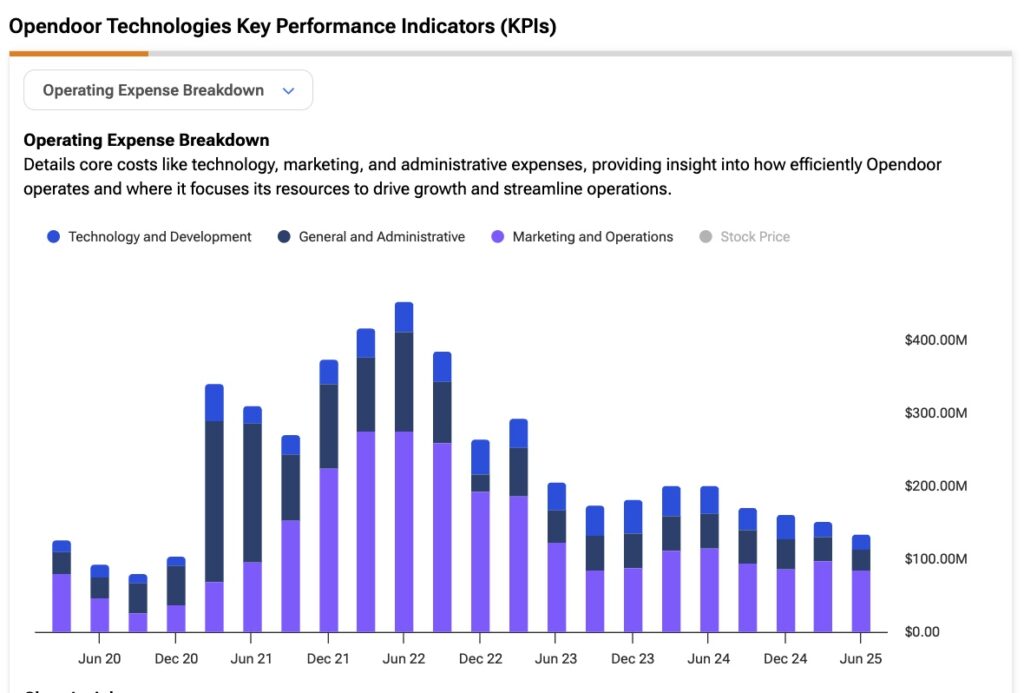

Beyond its booming appeal to retail investors, Opendoor, as a real estate technology company, is deeply tied to mortgage financing, which is directly linked to interest rates. The company’s core model revolves around buying homes, renovating them, and reselling them.

Naturally, lower rates reduce borrowing costs, which allows Opendoor to finance homes more cheaply and expand margins. Higher rates, on the other hand, squeeze profitability by driving up financing expenses.

Take the pandemic, for example: the Fed slashed rates and continued bond purchases (quantitative easing), which pushed U.S. mortgage rates down to roughly 2.7%-3.0%. That fueled housing demand, sent prices soaring, and helped Opendoor’s revenue jump from $2.5 billion in 2020 to $15.5 billion in 2022. The stock followed suit, peaking at nearly $35 in February 2021.

However, starting in 2022, inflation accelerated, reaching ~9% in June of that year—and the Fed quickly shifted into rate-hiking mode, raising rates to 5.5% by mid-2023. As borrowing costs surged, Opendoor’s revenues collapsed from $15.5 billion in 2022 to just $5.15 billion in 2024, with steep operating losses dragging the stock down to penny-stock levels by July. Even so, shares have since bounced more than 830% from those lows.

That rebound was fueled in part by retail investors and Eric Johnson of EMJ Capital, who laid out a super-bullish case: that Fed rate cuts would reignite housing demand and Opendoor’s iBuying model—now facing limited competition—could scale profitably as volumes return. And while Opendoor posted its first positive EBITDA quarter in three years during Q2, selling 63% fewer homes year-over-year (approximately 1,700), management was quick to caution that this EBITDA trend won’t hold, given the still-weak housing backdrop.

The Fed Pulls the Trigger, But OPEN’s Catalyst Needs Time

On September 17, the Federal Reserve cut rates by 25 basis points, exactly as the market expected. In theory, this was a key catalyst for Opendoor’s bullish thesis, even if it wasn’t a surprise. The stock even spiked as much as 20% during the session ahead of the official announcement.

Chart showing the price action of OPEN stock from September 12th to September 18th.

Still, the real focus wasn’t the cut itself, but what comes next. For the rest of 2025, six Fed officials don’t expect any more cuts, while nine others see room for two additional cuts—bringing the total to 50 bps. More importantly, the Fed shifted its attention to the job market, warning that downside risks to employment are rising. That message, coupled with a “meeting-by-meeting” approach going forward, quickly cooled market enthusiasm. OPEN still finished the day higher, but with a slightly smaller gain than its intraday peak.

Longer term, rate cuts (and the possibility of more to come) strengthen the bull case for OPEN. But in the short run, the housing market doesn’t move instantly. While lower mortgage rates immediately boost affordability, buyers usually need time to adjust plans. Historically, mortgage applications and pre-approvals pick up within 3-6 months after a 25-bp cut, while actual home sales and prices typically react over 6-12 months.

That timing lines up with what former CEO Carrie Wheeler—who stepped down in August under pressure from activist investors—warned in the Q2 shareholder letter: the back half of 2025 could remain tough, with few immediate catalysts following the “slowest spring selling season in thirteen years.”

Tracking Opendoor’s Next Move

The appointment of Kaz Nejatian, former COO of Shopify (SHOP), as Opendoor’s new CEO on September 10th was welcomed by the market, with OPEN shares hitting new highs for the year. Investors see his arrival as a signal of a strategic pivot toward a capital-light business model built on agent partnerships and recurring revenues.

While it will take time for this shift to be reflected in the numbers, the leadership change and clear direction alone have already revived momentum—especially since the old, capital-intensive model had been weighing on profitability.

More importantly, retail-driven hype fueled by rate cuts and fresh management is likely to keep bringing positive flows into the stock, supporting valuation while the new model takes shape. To put this in context, OPEN was trading at just 3.4x price-to-cash flow in mid-August but now sits at 12.5x—still 4% below the sector average.

That said, with valuations already re-rated and a blurry line between hype and fundamentals, I still think a safety net is essential for anyone betting on a turnaround. For those holding a long position, hedging with deep out-of-the-money puts is a smart way to add protection.

With the stock at $10, the idea could be buying $5.5 strike puts (roughly where shares traded in early September). This setup offers affordable protection against a major selloff while allowing me to capture the upside if momentum continues to build.

I would also suggest targeting an expiration just after the next earnings release on November 6th, since options markets are pricing in a 60.7% expected move based on the at-the-money straddle. That way, the hedge is in place for the most volatile window, when results or guidance could swing the stock dramatically.

Is OPEN Stock a Buy or Sell?

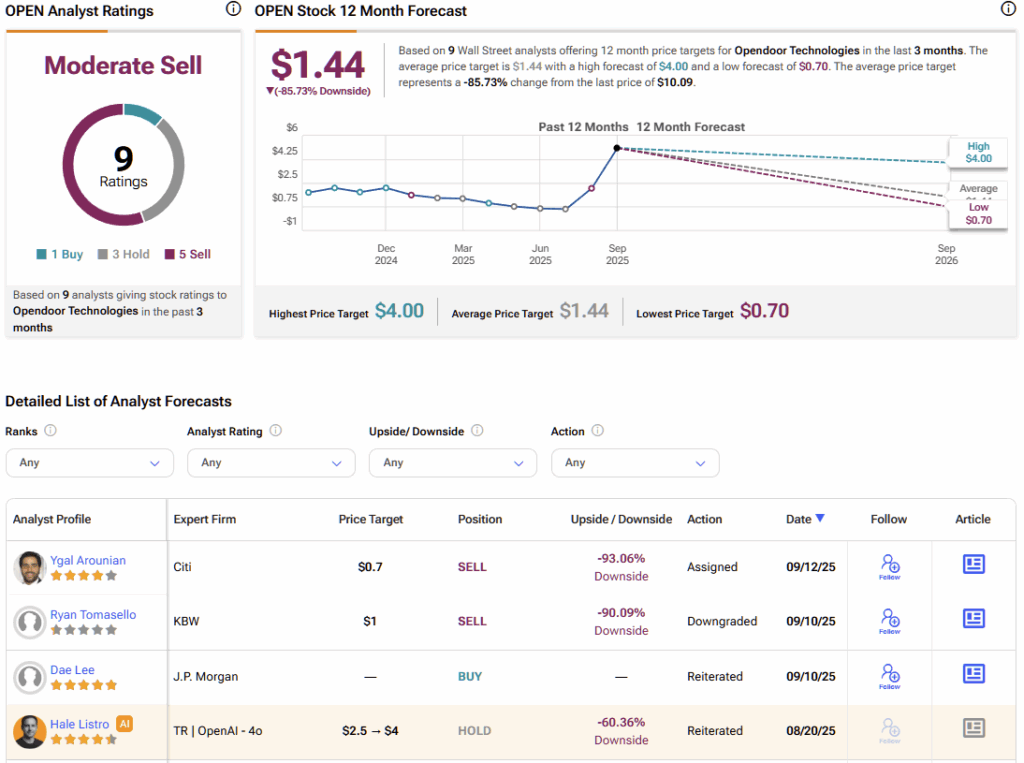

The analyst consensus on Opendoor is pretty bearish: out of nine covering the stock over the past three months, only one is a Buy, three are Holds, and five are Sells. The average price target stands at just $1.44, implying more than 85% downside from current levels over the coming year.

Opendoor remains a highly speculative stock—far from profitability, yet riding strong bullish momentum fueled by retail enthusiasm, rate cuts, and CEO change hype. At current valuations, I see OPEN more as trading material than a long-term hold. Option chains are already flagging elevated volatility heading into earnings.

Until then, it’s hard to see much derailing short-term retail optimism, unless Q3 results in November tell a different story. For this reason, I believe a speculative Buy rating is warranted, but paired with a risk-reduction strategy to guard against sharp pullbacks until earnings are reported.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Key Trends to Watch This Fall

Key Trends to Watch This Fall 1. Prices Up, But Homes Taking a Bit Longer to Move

1. Prices Up, But Homes Taking a Bit Longer to Move What This Means for Buyers & Sellers

What This Means for Buyers & Sellers Looking Ahead: What Could Tip the Balance?

Looking Ahead: What Could Tip the Balance?